Your salary is exactly what it was two years ago. Maybe you even got a small raise. But something feels wrong: by the third week of the month, your account is lower than it used to be at this point. You’re not spending more recklessly. So what’s happening?

You’re not imagining it. And the explanation involves several forces working simultaneously — most of which nobody talks about clearly.

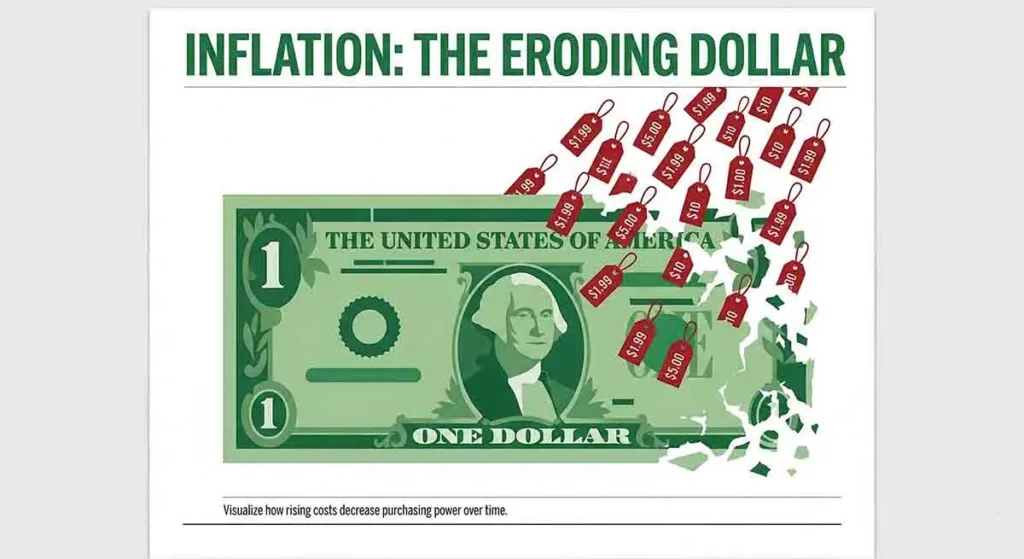

Inflation Is Eroding Your Real Wage

A salary of $60,000 in 2020 is not the same as $60,000 in 2026. Cumulative inflation over that period means your dollars buy significantly less. If your salary grew by 8% since 2021 but cumulative inflation ran at 20%+, you’re effectively taking a pay cut in real terms every year — even as your nominal salary stays flat or rises slowly.

This is what economists call real wage stagnation. Your paycheck number stays the same. What it can actually purchase contracts. The supermarket is the most visceral place this shows up — the same cart of groceries costs 25–40% more than it did four years ago.

Hidden Cost Increases You’re Not Tracking

The costs that sneak up on people aren’t usually the headline items. They’re the ones that increase a little, quietly, and don’t send a bill that demands attention:

- Auto insurance premiums — Up 20–35% in most states since 2022 due to repair costs and increased claims.

- Home/renters insurance — Climate-related claims have driven premiums up significantly nationwide.

- Utility bills — Electricity and gas costs have risen faster than CPI in most regions.

- Healthcare cost-sharing — Even if your premium stayed flat, co-pays, deductibles, and out-of-pocket maximums have crept upward.

- Interest on revolving debt — If you carry any credit card balance, today’s rates (averaging above 20% APR) mean significantly more of each payment goes to interest versus principal.

None of these feel dramatic month to month. Combined, they can quietly consume hundreds of dollars that used to be available for savings or discretionary spending.

Tax Bracket Creep

If you received any raise — even a modest cost-of-living adjustment — you may have moved slightly higher within your tax bracket, or even into the next one. This means a larger percentage of your income goes to federal and state taxes without any lifestyle improvement to show for it.

The IRS adjusts brackets annually for inflation, but if your employer’s raises lag behind inflation (which is common), you can end up in a slightly worse tax position even as your purchasing power shrinks.

The Subscription Drain

This one flies under the radar because each individual subscription seems minor. But subscription prices have increased substantially across nearly every platform since 2021: streaming services, music, cloud storage, news sites, software tools, gyms, meal kits.

A household that subscribed to Netflix, Spotify, iCloud, a gym, and two news sites in 2021 for roughly $80/month is likely paying $130–150/month today for the same services — a 60–80% increase on services most people barely notice on their bank statements.

What You Can Actually Do

- Run a real subscription audit. Export 90 days of bank/card statements and highlight every recurring charge. Most people find 3–5 subscriptions they forgot they have.

- Negotiate your insurance annually. Both auto and renters/home insurance are negotiable — call, tell them you’re shopping around, and ask for a loyalty discount. It works more often than people expect.

- Pay down high-interest debt first. At 20%+ APR, every dollar toward credit card principal is effectively a guaranteed 20% return on investment.

- Re-examine fixed expenses vs. variable. Rent, car payments, and insurance are the levers that matter most. Cutting lattes is real but marginal.

- Build the case for a real raise. If you’re more than 18 months past your last raise, you’re likely underpaid relative to the current market. Research comparable salaries and bring data to that conversation.

“The feeling that your money doesn’t go as far is not anxiety — it’s arithmetic. The math has changed. Your spending strategy needs to change with it.”

Leave a Reply