If you’ve ever looked closely at a month of bank and card statements, you’ve probably noticed charges you don’t remember signing up for. The average American household pays an estimated $300–$600 per year in fees that are technically disclosed but practically invisible — buried in terms, auto-renewed, or simply never cancelled after the initial signup.

Here’s the full map of where the money quietly goes.

Banking Fees — The Ones That Shouldn’t Exist Anymore

- Monthly maintenance fees ($12–$25/month): Many traditional banks still charge these unless you maintain a minimum balance or meet direct deposit requirements. If you’re paying this, switch to a credit union or online bank — many offer genuinely free checking.

- Out-of-network ATM fees ($3–$5 per transaction): Often double-charged — once by your bank, once by the ATM operator. Over 12 transactions a year, this can exceed $100.

- Overdraft fees ($25–$35 per incident): The CFPB has pushed back on these significantly and some banks have eliminated them, but many still charge. Opt-out of overdraft “protection” if you haven’t already — a declined card is better than a $35 fee.

- Paper statement fees ($1–$3/month): Banks charge for the convenience of receiving a physical record of your own money. Switch to electronic statements.

- Inactivity fees ($5–$15/month): Some accounts charge these if you haven’t used the account in 12 months. Worth reviewing any old accounts.

Subscription and Membership Traps

- Free trials that auto-converted: The most common hidden fees. The trial ended, the charge started, and you never noticed. Search your statements for charges under $20 from unfamiliar company names.

- Annual renewal bumps: Many services offer a low first-year price and auto-renew at full price. Common offenders: antivirus software, VPNs, app subscriptions, professional membership organizations.

- App store subscriptions: Apple and Google make it genuinely difficult to audit all active subscriptions. On iPhone: Settings → [your name] → Subscriptions. On Android: Google Play → Subscriptions. Most people find at least 2–3 surprises.

- Gym membership auto-renewals: “Cancel anytime” memberships that require certified mail or in-person cancellation to actually stop charging.

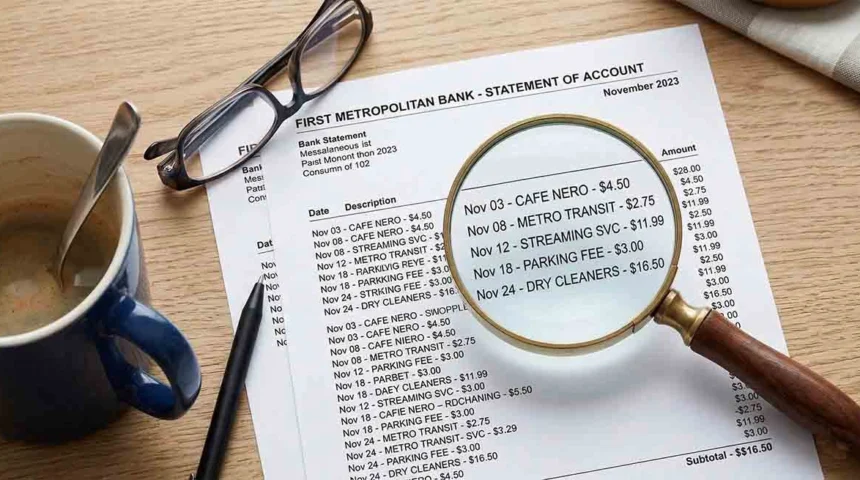

Quick win: Export 90 days of bank and card statements, highlight every recurring charge, and check every one you can’t immediately explain. This single exercise typically surfaces $30–$80/month in recoverable fees.

Insurance Add-Ons You Didn’t Know You Had

- Credit card payment protection insurance: Often enrolled at credit card signup, typically $0.89–$0.99 per $100 of balance. On a $5,000 balance, that’s $45–$50/month for insurance most people never use or need.

- Rental car insurance through dealerships: If you bought a car recently and accepted the dealer financing, you may have been enrolled in optional protection products that get added to your monthly payment.

- Phone carrier insurance: $15–$17/month per phone from most major carriers. If your phone is more than two years old, consider whether the replacement cost math still favors the insurance.

- Mortgage lender-placed insurance: If your homeowner’s insurance ever lapsed and your mortgage servicer enrolled you in their own policy, lender-placed insurance is typically 2–3x the cost of market-rate policies.

Telecom Junk Fees

FCC efforts to curb hidden telecom fees have had partial success, but several persist:

- “Administrative” and “regulatory recovery” fees: Not actually government-mandated. Added by carriers as profit padding. Typically $3–$10/month that advertised rates never mention.

- Equipment rental fees: If you’re renting a router or cable box from your ISP or cable provider, buying your own equipment typically breaks even within 6–12 months.

- Early termination fees embedded in promotional periods: Promotional rates that revert after 12 months — effectively a hidden price increase that was in the fine print of the contract.

How to Audit and Actually Recover Your Money

- The 90-day statement sweep: Export and review every charge under $30 on your bank and all card statements. These are the fee-sized amounts that individually feel too small to investigate but collectively are substantial.

- Call to cancel, then negotiate: Many services will offer a discount rather than lose you. “I’m calling to cancel” gets a different response than “I’m calling to ask for a discount.”

- Use Rocket Money, Trim, or similar apps: These scan your statements for recurring charges automatically and can cancel subscriptions on your behalf.

- Set calendar reminders for trial ends: Whenever you start a free trial, immediately set a calendar reminder for two days before the trial ends.

Leave a Reply