You want to buy a home. But there’s a real possibility — a job change, a relationship change, an opportunity — that you might not stay in this city for more than a few years. Every piece of real estate advice you’ve ever read says you need to stay at least 5 years to make buying worthwhile. Is that still true in 2026?

The honest answer: it depends on specifics that the generic advice doesn’t account for. Here’s the actual math.

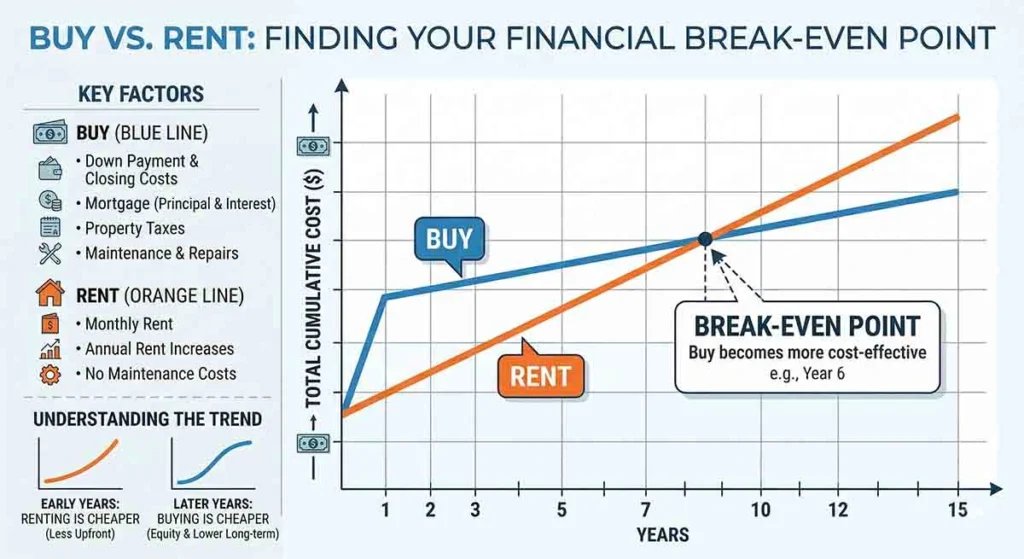

The Break-Even Calculation

The classic “5-year rule” exists because of transaction costs. Buying a home involves: closing costs (2–5% of purchase price), moving costs, and potential home preparation costs. Selling involves: realtor commissions (typically 5–6% combined buyer/seller), potential repairs or updates to prepare for sale, and closing costs again. Combined, transaction costs on a $400,000 home can run $40,000–$60,000.

For buying to beat renting financially, the home needs to appreciate enough (or generate enough equivalent savings vs. rent) to overcome these transaction costs. At historical appreciation rates of 3–4% annually, a $400,000 home gains $12,000–$16,000/year in value. Break-even on $50,000 in transaction costs: roughly 3–4 years at that appreciation rate. The “5-year rule” builds in a buffer for slower appreciation periods.

2026-Specific Factors That Change the Math

Mortgage rates: Rates above 6% (which have persisted since 2023) significantly increase monthly carrying costs relative to a comparable rental in many markets. The higher the rate, the larger the proportion of early mortgage payments that go to interest rather than building equity — lengthening the break-even timeline.

Price-to-rent ratios: In many metros, home prices remain elevated relative to rents — meaning the monthly cost of ownership (at current rates) substantially exceeds comparable rent. This increases the appreciation required to justify purchase over a short timeline.

Market trajectory: Markets where prices have softened from 2021–2022 peaks (many Sun Belt cities) offer different calculation inputs than markets that have remained stubbornly elevated (Northeast, coastal California).

Transaction Costs — The Real Killer for Short Stays

On a $450,000 home:

- Buying closing costs: ~$9,000–$18,000 (2–4%)

- Selling realtor commissions: ~$22,500–$27,000 (5–6%)

- Staging, minor repairs before sale: $3,000–$8,000

- Total transaction friction: ~$35,000–$53,000

At 3% annual appreciation, a $450,000 home gains ~$13,500/year. To cover $44,000 in average transaction costs through appreciation alone: 3.3 years — before accounting for the rate-driven carrying cost disadvantage vs. renting.

The Renting Alternative Analysis

The comparison isn’t “buy and build equity vs. rent and throw money away.” It’s “buy with X monthly cost and equity building vs. rent at Y monthly cost and invest the difference.” If renting the equivalent property costs $800/month less than ownership (principal, interest, taxes, insurance, maintenance), and you invest that $800/month over 3 years, you may come out ahead of the equity you’d build through homeownership at current rates during that period.

Run this comparison with actual numbers for your specific market before deciding.

The Decision Framework

Buying makes more sense over a 3-year horizon when:

- Monthly ownership cost is within $300–400 of comparable rent (rare at current rates but possible in some markets)

- You’re in a market with above-average appreciation trajectory

- You have strong reasons to believe you’ll stay or can easily rent the property if you leave

- The purchase is below your maximum qualification and leaves meaningful financial cushion

Renting makes more sense when:

- The price-to-rent ratio in your market is above 20 (compare annual rent to purchase price — if a $450,000 home rents for $18,000/year, ratio is 25)

- Monthly ownership cost would exceed comparable rent by more than $500

- Your plans are genuinely uncertain and the flexibility of renting has real value to your specific situation

Leave a Reply