The average emergency vet visit now runs $1,500–$3,000. A dog cancer treatment can exceed $10,000. Dental cleaning for a cat: $500–$1,200. And somewhere around 40% of American pet owners do not have pet insurance — either because they looked at the premiums and math didn’t work, or because they never got around to it.

When your pet needs care and your bank account doesn’t have thousands waiting, you need real options — not lectures about why you should have planned ahead.

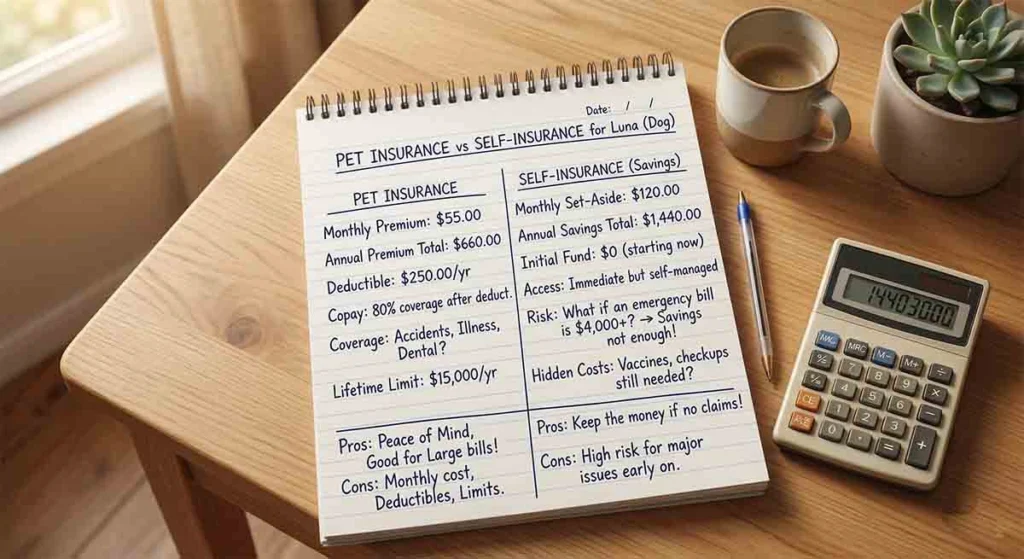

Is Pet Insurance Actually Worth It in 2026?

Pet insurance has become increasingly expensive in recent years as claim rates have risen and veterinary costs have increased. Average monthly premiums in 2026 run $40–$100/month for dogs and $25–$60 for cats, depending on breed, age, and coverage level. Over 10 years, that’s $4,800–$12,000 in premiums for a dog.

The break-even analysis depends entirely on your pet’s health trajectory. For breeds prone to expensive conditions (hip dysplasia, certain cancers, cardiac issues), insurance often pays for itself. For healthy mixed-breed pets with no genetic predispositions, many owners find that self-insuring — saving the equivalent premium into a dedicated pet emergency fund — leaves them ahead financially.

The honest answer: If you cannot afford to pay a $3,000 vet bill out of pocket and would not be able to build a $3,000 emergency fund within 2 years, insurance is probably worth the cost. If you could build that fund, self-insurance may be the better math.

Financing Options That Work

- CareCredit: A medical credit card accepted at most veterinary practices, offering 6–24 month zero-interest promotional periods if paid in full. Genuinely useful for unexpected large bills — just watch the standard APR if you don’t pay within the promotional window.

- Scratchpay: Pet-specific financing company, often available through vet offices. More flexible approval criteria than traditional credit.

- Payment plans directly from your vet: Many veterinary practices — especially independent ones — will create informal payment plans for established clients. This requires asking directly, but more vets offer this than advertise it.

- Personal loans: For large bills, a personal loan at 8–15% APR beats a credit card at 24%+ substantially.

Low-Cost Vet Options Most People Don’t Know About

- Veterinary school teaching clinics: Accredited veterinary schools (most states have at least one) operate teaching clinics where supervised students provide care at 40–70% below market rate. Quality is rigorously overseen by licensed veterinarians.

- Humane society and SPCA clinics: Many shelters run low-cost veterinary clinics open to the public, not just shelter animals. Services are typically limited but include vaccinations, basic wellness, and sometimes dentals.

- Non-profit vet organizations: Organizations like the ASPCA in New York, Pets of the Homeless nationally, and many regional nonprofits provide subsidized care based on income.

- Banfield (PetSmart) wellness plans: Monthly subscription-based model that covers preventive care — annual exams, vaccines, routine lab work — at a fixed monthly cost. Not insurance, but useful for predictable preventive expenses.

Prevention Math: What’s Worth Spending On

The best financial strategy is spending on prevention that prevents expensive treatment:

- Annual dental cleanings ($300–$600) prevent periodontal disease that, if untreated, can lead to organ damage costing thousands more.

- Monthly heartworm prevention ($5–$15/month) prevents heartworm treatment ($1,000–$3,000).

- Weight management — obese pets have dramatically higher rates of diabetes, joint disease, and cardiac issues. Keeping your pet at healthy weight is the single highest-ROI health intervention available.

- Regular vet visits catch problems when they’re inexpensive to treat rather than expensive to manage.

Can You Negotiate Vet Bills?

Yes — more often than most people realize. A few specific approaches:

- Ask for an itemized estimate and ask what’s absolutely necessary vs. optional to defer.

- Tell your vet your financial constraints directly: “I can spend $X today — what’s the most important thing to address with that?”

- Ask whether generic medications can substitute for branded ones (often yes, at dramatically lower cost).

- For non-emergency situations, ask whether any planned procedures can wait until you have more time to save or compare prices.

Leave a Reply