Tax season arrives every year and millions of Americans face the same quiet dread — the return is not done, the deadline has passed, or the situation feels too complicated to face. If you are asking yourself what happens if I don’t file my taxes, you are not alone. The IRS receives approximately 160 million individual returns each year, and a significant number arrive late, incomplete, or not at all.

This guide gives you the complete, honest picture — every penalty, every consequence, every timeline, and every legitimate option for getting back on track. Whether you missed this year’s deadline, have not filed in several years, or are trying to understand the difference between not filing and not paying, everything you need to know is here.

2026 Tax Deadlines — The Dates That Matter

For the 2025 tax year, the federal filing deadline is April 15, 2026. If you need more time to prepare your return, you can file for an automatic six-month extension, which moves your filing deadline to October 15, 2026. Critically, the extension gives you more time to file — it does not give you more time to pay. Any tax owed is still due on April 15, 2026, regardless of whether you file an extension.

If you are owed a refund and have not filed, you have until April 15, 2029 to claim it (three years from the original deadline). After that date, the IRS permanently keeps your refund. No exceptions, no appeals.

According to the IRS Topic 653 on penalties and interest, the clock on penalties starts running the day after the filing deadline — and it does not stop until you file and pay what is owed.

The Failure-to-File Penalty — What It Costs You

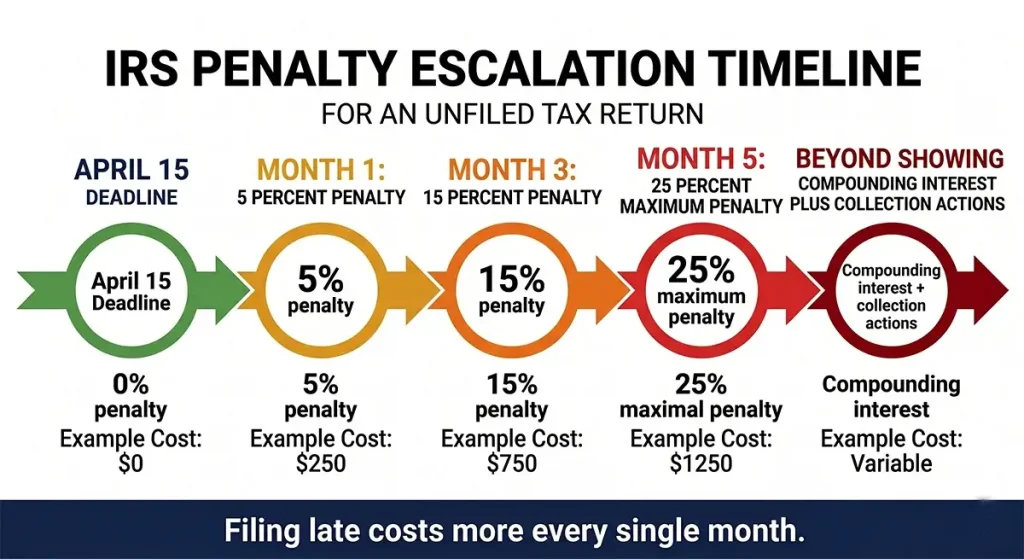

The failure-to-file penalty is the most expensive tax penalty most Americans will ever encounter. Here is exactly how it works in 2026:

- Rate: 5% of your unpaid tax for each month (or partial month) your return is late

- Maximum: 25% of your unpaid tax (reached after 5 months)

- Minimum penalty (after 60 days late): The lesser of $525 or 100% of your unpaid tax — whichever is smaller

Let us make this concrete. Suppose you owe $5,000 in taxes and do not file your return:

- After 1 month: $250 penalty (5% of $5,000)

- After 3 months: $750 penalty (15%)

- After 5 months: $1,250 penalty (25% — the maximum)

A $5,000 tax bill becomes a $6,250 obligation in just five months — before interest, before the failure-to-pay penalty, before collection costs. For a $20,000 tax liability, the maximum failure-to-file penalty alone adds $5,000 to what you owe.

The minimum penalty deserves special attention. If you file your return more than 60 days after the deadline and you owe any taxes, the IRS will charge you at least $525, even if your actual tax bill is only $100. The minimum penalty in this case would be $100 (100% of what you owe, since that is less than $525), but the point remains: there is a floor, and it is not small.

“The failure-to-file penalty is designed to be punishing — and it is. At 5% per month it accumulates ten times faster than the failure-to-pay penalty of 0.5% per month. This is why filing on time, even when you cannot pay, is one of the most financially important decisions a taxpayer can make.”

The Failure-to-Pay Penalty — A Separate Problem

Even if you file your return on time, if you do not pay what you owe by the deadline, a separate penalty begins:

- Rate: 0.5% of your unpaid tax for each month (or partial month) the balance remains unpaid

- Maximum: 25% of your unpaid tax (reached after approximately 50 months)

- Reduced rate: If you have an IRS-approved installment agreement, the rate drops to 0.25% per month

- Increased rate: After an IRS levy notice, the rate increases to 1% per month

When both penalties apply in the same month, the failure-to-file penalty is reduced by the failure-to-pay amount. So instead of 5% failure-to-file plus 0.5% failure-to-pay (5.5% total), you pay 4.5% failure-to-file plus 0.5% failure-to-pay — still 5% total but properly allocated between the two penalties.

The maximum combined penalty exposure is significant: up to 25% from failure-to-file plus up to 25% from failure-to-pay — potentially adding 47.5% to your original tax bill, before interest. According to the IRS failure-to-pay penalty page, these charges compound until the balance is fully paid.

Interest — The Silent Cost That Never Stops

In addition to both penalties, the IRS charges interest on any unpaid balance starting the day after the original filing deadline. As of the fourth quarter of 2025, the interest rate for individuals is 7% annually — calculated as the federal short-term rate plus 3 percentage points, adjusted quarterly.

Interest compounds daily. Unlike penalties, which have caps and can sometimes be waived, interest accrues continuously and cannot be forgiven through abatement processes. Even if the IRS removes all your penalties for reasonable cause, the interest keeps running.

Here is the real-world compounding effect on a $10,000 unpaid tax balance at current rates:

- Year 1: ~$700 in interest alone (before penalties)

- Year 3: ~$2,200 in compounded interest

- Year 5: ~$4,000 in compounded interest

When you add the failure-to-file penalty (maxing at $2,500 after 5 months) and failure-to-pay penalty (continuing to grow at 0.5% per month), a $10,000 tax obligation left unaddressed for five years can grow to $17,000–$20,000 — nearly double the original amount owed.

What Happens If You Are Owed a Refund

Here is the good news that most people in this situation do not realize: if the IRS owes you money, there is no penalty for filing late. The failure-to-file and failure-to-pay penalties only apply when you owe tax. If you are getting a refund, the only consequence of filing late is potentially losing your refund if you wait too long.

Approximately 75% of Americans receive a refund each year. If you have not filed but are due a refund, you have three years from the original deadline to claim it. For your 2025 taxes, that window closes on April 15, 2029.

After three years, the unclaimed refund is permanently forfeited to the U.S. Treasury. The IRS does not automatically send it to you — you must file the return to receive it. In 2024, the IRS reported that approximately $1.5 billion in refunds went unclaimed because taxpayers did not file within the three-year window.

If you have not filed in multiple years and are unsure whether you owe or are owed money, you can request a Wage and Income Transcript from the IRS (Form 4506-T) which shows all income reported to the IRS under your Social Security number — this lets you estimate your tax position before spending money on professional preparation.

The IRS Substitute for Return — When the IRS Files for You

Many Americans assume that not filing means the IRS simply does not know about their income. This is a dangerous misconception. When you do not file, the IRS does not sit idle. Employers, banks, brokerages, and other payers report your income to the IRS on W-2s, 1099s, and other information returns. The IRS has your income data whether you file or not.

When an IRS notice requesting a return goes unanswered, the IRS can prepare and file a Substitute for Return (SFR) on your behalf under IRC Section 6020(b). Here is what makes this consequential:

- The IRS only includes income it can document — it does not add any deductions, credits, or exemptions beyond the standard deduction

- This means an SFR almost always results in a higher tax liability than a properly filed return would show

- Self-employed individuals lose all business deductions — the IRS sees gross revenue, not net profit

- You lose the ability to claim Earned Income Credit, Child Tax Credit, education credits, and other refundable credits you may be entitled to

Once an SFR is filed, the IRS will send you a Notice of Deficiency (CP2000 or a 90-day letter). You have 90 days to respond. If you do not respond, the tax assessed in the SFR becomes final, the IRS adds penalties and interest from the original due date, and collection actions can begin.

The critical point: even after an SFR is filed, you can still file your own actual return to replace it — and doing so almost always results in a lower tax liability because you can claim all legitimate deductions and credits.

IRS Collection Actions — Liens, Levies, and Wage Garnishments

If you have unfiled returns or unpaid taxes and ignore IRS notices, the agency has substantial legal power to collect what it is owed. Understanding this timeline matters:

The IRS Notice Sequence

- CP14 — Balance Due Notice: Your first notice informing you that you owe taxes

- CP501/CP503 — Reminder Notices: Follow-up reminders escalating in urgency

- CP504 — Intent to Levy Notice: A serious warning that the IRS plans to seize property

- LT11 / Letter 1058 — Final Notice of Intent to Levy: Your legal right to appeal (Collection Due Process hearing) is triggered here — this is your last formal opportunity to dispute or negotiate before enforcement

Federal Tax Lien

Once you have an assessed, unpaid tax debt and ignore a Demand for Payment, the IRS can file a Notice of Federal Tax Lien. This is a public legal claim against all of your property — real estate, vehicles, financial accounts, and future property acquired while the lien is active. The lien:

- Damages your credit score significantly

- Attaches to your home — preventing you from selling or refinancing without first paying the tax debt

- Is publicly recorded in your county and searchable by lenders, employers, and business partners

- Remains until the debt is paid or becomes uncollectible (generally after 10 years)

Tax Levy and Wage Garnishment

A levy is the actual seizure of property — more serious than a lien. The IRS can levy:

- Bank accounts: A bank levy freezes and seizes funds in your account up to the amount you owe. You have 21 days after the freeze to resolve the issue before the bank sends the money to the IRS.

- Wages (wage garnishment): The IRS can require your employer to withhold a portion of every paycheck until the debt is paid. Unlike most creditor garnishments, the IRS wage garnishment formula allows them to take significantly more than other creditors — often leaving taxpayers with only a modest exempt amount each pay period.

- Social Security benefits: The Federal Payment Levy Program allows the IRS to take up to 15% of your Social Security retirement and disability benefits.

- Tax refunds: Future refunds are automatically applied to unpaid balances before you receive anything.

Passport Revocation — The Consequence Most Americans Do Not Expect

Under the FAST Act (Fixing America’s Surface Transportation Act) passed in 2015, the IRS has the authority to certify taxpayers with “seriously delinquent” tax debt to the U.S. Department of State, which can then deny a passport application or revoke an existing passport.

For 2026, the seriously delinquent threshold is $66,000 — this includes taxes, penalties, and interest combined. This figure is inflation-adjusted annually.

If you receive a CP508C Notice from the IRS, your tax debt has been certified to the State Department. Your passport may be revoked within weeks. If you are abroad when this happens, you may be issued only a limited passport permitting your return to the United States — not ongoing international travel.

The passport restriction is lifted when:

- The debt is paid in full

- An IRS installment agreement is approved and payments are current

- An Offer in Compromise is accepted

- The debt is placed in Currently Not Collectible status

Importantly, if the IRS filed a Substitute for Return for you and you never responded, your balance may have grown beyond the $66,000 threshold without you realizing it — making passport revocation a real possibility even for people who simply stopped filing and assumed the problem went away.

When Does Not Filing Become a Crime?

This is the question most people are really asking, and the honest answer requires distinguishing between civil consequences (which apply to essentially everyone who does not file) and criminal consequences (which are far less common but genuinely serious).

Civil vs. Criminal Tax Matters

The vast majority of people who do not file taxes face civil penalties — fines, interest, collection actions. These are financial consequences, not criminal charges. The IRS resolves over 99% of non-filing situations through civil channels.

Criminal charges require the government to prove willfulness — that you deliberately and intentionally avoided filing or paying taxes. Simply forgetting, being confused by the tax code, or being in financial distress is not willful — it is civil. Deliberately hiding income, destroying records, or repeatedly ignoring IRS notices after being warned can demonstrate willfulness.

Failure to File — Misdemeanor

Under 26 USC §7203, willful failure to file a return is a federal misdemeanor punishable by:

- Up to $25,000 in fines

- Up to one year in federal prison

- Plus the cost of prosecution

Tax Evasion — Felony

Under 26 USC §7201, willful tax evasion — which can include a pattern of non-filing combined with deliberate concealment — is a federal felony punishable by:

- Up to $100,000 in fines for individuals ($500,000 for corporations)

- Up to five years in federal prison

- Full repayment of all taxes, penalties, and interest

The IRS Criminal Investigation Division (CID) maintains a 90% conviction rate — but this statistic is often misunderstood. It reflects the IRS’s highly selective prosecution strategy: they only bring criminal cases they are extremely confident of winning, typically involving egregious, documented willfulness. In FY2025, the IRS CID identified $4.5 billion in tax fraud and referred approximately 2,600 cases for prosecution — out of 160+ million filers.

Most people who do not file taxes will never face criminal prosecution. But the risk increases significantly if you: ignore multiple formal IRS notices, have clearly reportable income that you are concealing, are a business owner failing to file payroll tax returns, or demonstrate a pattern suggesting deliberate evasion.

What Happens When You Have Not Filed for Multiple Years

Multiple years of unfiled returns creates a compounding problem that many people feel paralyzed by. Here is the reality of the situation:

How Many Years Does the IRS Require?

The IRS generally requires taxpayers who have not filed to file the previous six years of returns to get into compliance. This is the IRS’s internal policy under the Internal Revenue Manual. In some cases — particularly for taxpayers with large balances or business tax issues — additional years may be required.

Statutes of Limitations

- IRS has no statute of limitations on unfiled returns. For any year you did not file, the IRS can assess tax at any time — the normal 3-year assessment window only starts running when a return is filed.

- 6-year assessment period: For filed returns where you underreported income by more than 25%, the IRS has six years to assess additional tax.

- No statute of limitations for fraud: If the IRS can prove fraudulent intent, they can go back indefinitely.

- 10-year collection statute: Once a tax is assessed (including via SFR), the IRS generally has 10 years to collect it before the debt becomes legally uncollectible.

The Cascade Effect on Penalties

Each unfiled year generates its own set of penalties. If you have not filed for five years and owe tax each year, you are potentially facing the maximum 25% failure-to-file penalty on five separate tax balances — in addition to failure-to-pay penalties and compounding interest on each. The total financial exposure can be staggering and often exceeds what the person could reasonably pay — which is why professional negotiation of these cases matters.

Your Options — How to Fix This

The single most important thing to understand: the IRS has seen every possible non-filing situation, and there is a structured path forward for each one. The people who end up with the worst outcomes are those who ignore the problem — not those who engage with it.

Option 1 — File Immediately and Pay in Full

If you can file your return and pay the full balance due (including any penalties and interest), this is always the cleanest resolution. Your account is resolved, no further collection action occurs, and you may be eligible to request penalty abatement.

Option 2 — File and Set Up an Installment Agreement

If you cannot pay in full, file your return and apply for an installment agreement. The IRS Online Payment Agreement tool allows you to set up monthly payments for balances under $50,000. Benefits of an approved installment agreement:

- Stops enforced collection actions (levies, garnishments)

- Reduces failure-to-pay penalty rate from 0.5% to 0.25% per month

- Keeps your passport safe (provided balance is below $66,000)

Option 3 — Offer in Compromise

An Offer in Compromise (OIC) allows qualifying taxpayers to settle their tax debt for less than the full amount owed. The IRS considers your ability to pay, income, expenses, and asset equity. OIC approval rates are not high (approximately 30-40% of submitted offers are accepted) but when approved, they can produce dramatic reductions in total liability. The pre-qualifier tool at IRS.gov can show you whether you are likely eligible.

Option 4 — Currently Not Collectible Status

If you genuinely cannot pay anything toward your tax debt — your income covers only basic living expenses — the IRS can place your account in “Currently Not Collectible” (CNC) status. Collection efforts pause. The 10-year collection statute continues running. This is not forgiveness, but it provides relief while your financial situation is genuinely difficult.

Option 5 — Penalty Abatement

If the penalties are a significant portion of what you owe, you may qualify to have them reduced or eliminated. This is covered in detail in the next section.

Penalty Abatement — How to Get Penalties Reduced or Removed

Penalties are not always permanent. The IRS has two primary mechanisms for reducing or eliminating assessed penalties:

First-Time Penalty Abatement (FTA)

First-Time Abatement is the IRS’s administrative waiver for taxpayers who have a clean penalty history. To qualify:

- You must have filed all required returns (or have a valid extension)

- You have not been assessed a penalty in the prior three tax years

- You have paid, or arranged to pay, all currently owed tax

FTA can be requested by calling the IRS directly at 1-800-829-1040 or by submitting Form 843. It is the easiest abatement to obtain and can remove failure-to-file and failure-to-pay penalties entirely for the affected year.

Reasonable Cause Abatement

If you do not qualify for FTA, you may still be able to remove penalties by demonstrating “reasonable cause” — circumstances outside your control that prevented timely filing or payment. The IRS accepts reasonable cause arguments for situations including:

- Serious illness or incapacitation (yours or an immediate family member’s)

- Death of a family member during the filing period

- Natural disaster affecting your ability to file

- Erroneous advice received from a tax professional

- Records destroyed in a fire, flood, or theft

The standard is genuine inability — not inconvenience. Document everything: medical records, death certificates, disaster declarations, or professional correspondence. Submit your reasonable cause argument in writing with the supporting documentation attached.

The Action Plan: What to Do Right Now

If you are reading this because you have not filed and do not know where to start, here is the practical sequence:

- Do not panic — but do not wait either. Every day you wait adds more interest to your balance. The problem does not improve with inaction.

- Determine which years you have not filed. Check your IRS account at IRS.gov/account where you can see your filing history and any balances under your Social Security number.

- Request income transcripts for each unfiled year. Use Form 4506-T or the IRS online transcript tool. These show all income reported by your employers and payers — essential for reconstructing past returns.

- Assess whether you owe or are owed a refund. For years where you are owed a refund, file immediately to claim it before the three-year window closes. For years where you owe, continue to the next steps.

- File every required return — starting with the most recent. Bringing your filing current is the first requirement for any IRS resolution program. File even if you cannot pay.

- Respond to every IRS notice. Ignoring official IRS notices accelerates the enforcement timeline and eliminates your formal appeal rights. Each notice has a response deadline — missing it costs you options.

- Consider professional help for complex situations. If you have multiple unfiled years, large balances, business tax issues, or received a criminal investigation referral, a tax attorney or enrolled agent (EA) is worth the cost. A qualified professional can negotiate directly with the IRS and often achieves substantially better outcomes than self-representation.

Filing Thresholds — Do You Actually Have to File?

Not everyone is required to file. For tax year 2026, the standard deduction thresholds roughly correspond to the filing requirements:

- Single filer under 65: Must file if gross income exceeds approximately $16,100

- Married filing jointly, both under 65: Must file if gross income exceeds approximately $32,200

- Head of household under 65: Must file if gross income exceeds approximately $24,150

Even if you are below these thresholds, you must file if you had self-employment income over $400, received certain types of income, or wish to claim refundable credits like the Earned Income Tax Credit.

Free Filing Resources

If cost has been a barrier to filing, the IRS Free File program offers no-cost federal tax preparation software for taxpayers with adjusted gross income of $84,000 or below. The Volunteer Income Tax Assistance (VITA) program provides free in-person tax help at thousands of community locations for eligible taxpayers. Both are legitimate, IRS-sponsored resources.

The Bottom Line

Not filing your taxes starts an escalating chain of consequences — penalties, interest, IRS collection actions, potential passport issues, and in serious cases, criminal liability. The consequences compound with every passing month. But every consequence described in this article is also stoppable. The IRS has formal, structured programs for every situation: installment agreements for people who cannot pay in full, Offers in Compromise for people in genuine financial hardship, Currently Not Collectible status for people with no ability to pay, and penalty abatement for people with clean prior histories or legitimate cause.

The Americans who end up with the worst outcomes are not those with the largest tax bills — they are those who stayed in avoidance longest. Filing a late return today is always better than filing it tomorrow. Engaging with the IRS, even from a difficult position, produces better results than ignoring them.

For official IRS guidance on your specific situation, the most authoritative starting point is IRS Topic 653 — Penalties, Interest, and IRS Notices, which covers all penalty types and your rights as a taxpayer. For payment options and installment agreements, visit the IRS Online Payment Agreement application directly.

Leave a Reply